AI and the Activation of Latent Markets

Recent advances in generative and agentic AI make one specific thing possible that wasn't before: effectively serving customers whose demand was always real but whose economics never worked at venture scale. The Big Bottom maps these structurally underserved segments at the base of every industry vertical — and charts why activating them requires agentic operations, precise positioning, and community-based distribution to compound in parallel.

Audio Transcript

AI and the Activation of Latent Markets

Something interesting is happening at the bottom of markets because of the recent advances in modern generative and agentic AI, and it's worth taking seriously. Not because AI makes everything possible, but because it makes one specific thing possible that wasn't before: effectively serving customers whose demand was always real but whose economics never worked at venture scale.

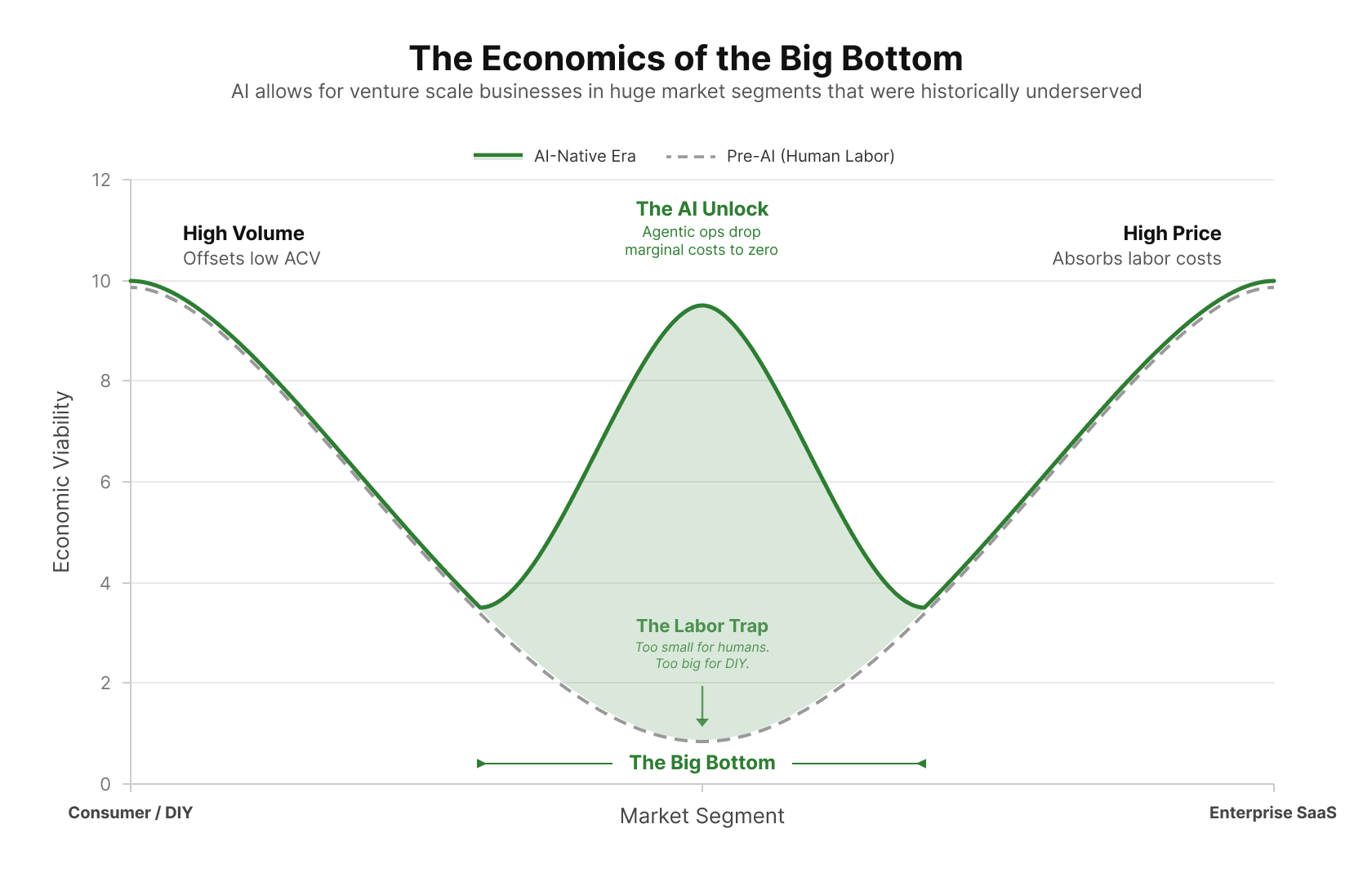

The gray dashed curve shows traditional service economics: viable at the extremes, collapsed in the middle. The green W-curve shows what happens when AI drops marginal cost of service delivery toward zero — the Big Bottom flips from the worst segment to the best.

We call this The Big Bottom (bot-tom, if you like: total obtainable market, unclaimed, at the base of every vertical). The term describes the large, structurally underserved segments sitting at the base of almost every industry vertical. These are customers who need the same things enterprise clients need: HR systems, legal support, operations software, financial infrastructure. The difference is that nobody ever built a profitable business serving them at scale, because the cost structure made it uninvestable. Too small to justify a sales team. Too scattered to serve efficiently. Too price-sensitive to absorb the overhead of onboarding and support.

That's a narrow claim, and I want to be precise about it. This isn't an argument that AI solves all problems at the bottom of the market. It's an argument that a specific constraint, the labor cost of most service delivery, has been structurally removed, or at the very least reduced significantly, because of modern AI. In certain market conditions, this change creates genuinely new opportunities to build business. And many of them are now venture-scale businesses as a result.

But cheaper delivery alone doesn't activate a market. Getting customers to arrive, to recognize themselves in what you're offering, requires something harder.

The Non-Consumption Problem

Economists have a term for what's happening here: non-consumption. These are markets where demand exists but the product or service has never reached the customer. Not because they don't want it, but because nobody could serve them profitably.

Consider the owner of an eight-person HVAC company who needed scheduling software, job costing, and a customer communication system years ago. The products existed. The implementation required a $12,000 contract and three months of onboarding. She used a spreadsheet instead. Or the freelance immigration consultant who needed contract templates, compliance tracking, and a client portal, but whose margins couldn't absorb law firm rates or a full-time operations hire. She got by with PDFs and a shared Google folder. Or Paws en Route, a pet travel company in the Hillock portfolio. They had the expertise and customer demand to grow into a real business. What they lacked was the operational infrastructure to handle the regulatory complexity of international pet travel at scale. Nothing on the market fit.

These customers didn't go without because the solution didn't exist. They went without because the solution required human labor to deliver, and the math didn't work at their price point.

Christensen's jobs-to-be-done framework describes this precisely: there's a job to be done — manage international pet travel logistics, run scheduling for an eight-person HVAC company — the customer has it, and no affordable solution gets hired to do it. The job goes undone, or done badly with whatever is available. That's the non-consumption market.

It's worth distinguishing this from his disruption theory, which describes companies entering at the low end and moving upmarket over time. The Big Bottom thesis doesn't follow that path. The economics of the middle segment, once AI drops the cost of delivery, are not a stepping stone to enterprise — they may be more attractive than enterprise outright. The goal isn't to build cheap and eventually move up. It's to build for a segment that is now structurally the best place to be. Incumbents don't retreat from these customers because of competitive pressure. They never served them in the first place. The opportunity sits in plain sight, consistently ignored, because the cost structure made it uninvestable.

AI changes the cost structure. When the marginal cost of service delivery approaches zero, non-consumption markets become consumption markets. That's not a small shift. That's the activation of a large latent demand that has been sitting dormant for decades.

What AI Actually Enables, And What It Doesn't

It's worth being precise about the mechanism, because the vague claim that "AI reduces costs" undersells the specific thing that's changing.

The traditional service business required humans at every link in the chain: to sell, to onboard, to deliver, to support, to retain. Add AI to speed up individual tasks and you get a more efficient human operation, but you still scale linearly, because humans are still doing the work. That's the copilot model: better tools for professionals, but the same fundamental cost structure underneath.

The shift that matters is architectural. Sequoia has written about this as the move from copilots to autopilots, from software that assists humans to software that delivers outcomes directly. In the autopilot model, the AI agent owns the goal, not just a step in the process. Humans shift from doing the work to supervising and improving the system. One person overseeing fifty agents is a fundamentally different cost structure than one person doing fifty tasks.

This matters for the bottom of the market because it changes what personalization means. Traditional service businesses personalized through human attention: expensive, unscalable. AI-native services can personalize through data and context at the point of delivery, across thousands of customers simultaneously, without proportionally increasing cost. The hyper-personalization that was once the exclusive advantage of high-cost, high-touch services becomes available at the bottom of the market.

That's genuinely new. It isn't just cheaper service. It's better service for customers who've never had access to it before. The techno-utopian in me loves the idea that technology distributed through the internet makes entirely new business possible and allows more of the population to experience things once only the privilege of the elite.

But it solves only the delivery side. Getting customers to recognize that a solution exists, and that it's for them, is a separate problem entirely.

Positioning Is How Markets Activate

There's a subtlety inside that problem that deserves its own treatment.

April Dunford, who has spent her career studying why great products fail to reach the customers they're built for, makes a distinction that matters enormously here. Most companies don't have a sales problem or a marketing problem. They have a positioning problem. They have the right features in the wrong order. They're speaking to the right audience in the wrong language. They're leading with what they built when they should be leading with the pain they solve.

In an established market, bad positioning means a potential customer goes to a competitor. You lose the deal, but the customer was already in motion: already aware they had a need, already shopping for a solution. The damage is bounded.

In a non-consumption market, bad positioning means something worse. The potential customer never tries you in the first place. They don't self-identify as someone with a solvable problem. They scroll past your message, file it under "not for me," and go back to living with the pain, because nothing you said connected your solution to their world.

This means positioning in these markets isn't a marketing function. It's the mechanism by which latent demand becomes active demand. Without it, the market doesn't activate. You can have the right product, the right price, the right operations, and still fail entirely. Not because customers tried you and left, but because they never arrived.

The implication for how you build is significant. You need to understand your target customer's world at a level of intimacy that lets you name their unarticulated pain before you pitch your solution. At Paws en Route, that meant not leading with "AI-assisted pet travel logistics" but with something far more specific: the dread of arriving at the airport with your dog and discovering the paperwork is wrong. International pet travel is governed by IATA live animal regulations that vary by carrier, destination country, and breed — regulations that change, that most pet owners only discover too late, and that no amount of Googling reliably resolves. That's the anxiety that unlocks recognition. The former describes the service. The latter describes the moment every client is trying to avoid.

And positioning, done at this depth, is genuinely hard to replicate. A competitor who copies your operations stack in eighteen months still has to do the same patient, ethnographic work with customers that you've already done. They can copy the product. They cannot easily copy the understanding of how your customer thinks about their own problem, or the trust that comes from having consistently spoken to them in a way that made them feel seen. Which is why getting the positioning right isn't just a prerequisite for reaching customers — it's also the precondition for the distribution that scales them.

The Acquisition Problem Is the Real Constraint

Here's where I want to be honest about something the enthusiasm around this thesis often skips: cheaper service delivery doesn't automatically create a venture-scale business. The cost-to-serve falling is necessary but not sufficient.

The harder problem is acquisition.

Getting to a million customers paying fifty dollars a month requires not just serving them cheaply, but finding them, convincing them, and keeping them at a cost that still leaves margin. Customer acquisition at the bottom of the market is not cheap just because AI exists. And small businesses churn. They close. They switch on price. They don't have procurement teams evaluating long-term vendor relationships.

But not all customers at the bottom are equally volatile. The churn problem is real for commodity buyers — customers with low operational complexity who switch on price because your service hasn't embedded itself in how they work. The customers worth building for are different: operationally complex businesses where your service has replaced a process, not just provided a tool. When an AI system has processed hundreds of a customer's transactions, learned their compliance edge cases, and accumulated context about what good judgment looks like in their specific operation, switching costs emerge that have nothing to do with features or price. Sequoia's services-as-software thesis makes this explicit: autopilot-model services begin compounding proprietary domain knowledge that deepens retention in ways a SaaS subscription doesn't. The solution to churn isn't better distribution. It's selecting for customers whose operational complexity makes the accumulation of that context genuinely valuable to them.

This is the strategic crux of the whole thesis. The companies that actually build venture-scale businesses in these markets won't just be the ones that figured out agentic operations or precise positioning. They'll be the ones that built durable, scalable distribution that works at the bottom. That's where the real defensibility comes from.

What do those distribution channels look like? Vertical communities, the associations, networks, and peer groups that already organize small businesses in specific industries, are natural rails. Unlike enterprise sales, where you negotiate with procurement, you earn trust from practitioners and let word of mouth do the work. Marketplaces and platforms where small businesses already transact are another lever. And product-led growth that generates visible value quickly, reducing the sales cycle that typically makes bottom-of-market unit economics difficult.

This is also where distribution and positioning reinforce each other. Vertical communities are places where context is already established. When a message reaches someone through a trusted peer in their specific world, the self-identification problem is partly solved before you've said a word. The channel does positioning work. Which is why the companies that earn deep community trust aren't just winning distribution. They're winning the right to be heard by customers who wouldn't have listened otherwise — and building the kind of defensibility that becomes harder to dislodge over time.

Why Defensibility Is Harder Than It Looks, And Where It Actually Comes From

The other honest acknowledgment: if AI makes the bottom of the market cheap to serve, it does so for everyone. The same technology that unlocks these markets for you is available to every competitor.

But a prior question sits underneath the defensibility argument: why do you get to be the one who accumulates it? If AI makes the bottom of the market cheap to serve on day one, a well-capitalized competitor can enter the same vertical with the same technology. The answer is that the race is won before the product ships. The ethnographic work required to achieve precise positioning — understanding how customers think about their own pain before you pitch a solution — is a non-purchasable asset. A competitor who arrives eighteen months later can hire engineers to replicate your operations stack. They cannot replicate what you learned from the first two years embedded in a specific vertical community, or the trust that comes from having consistently spoken to customers in a way that made them feel seen. Vertical communities are skeptical of late entrants in proportion to how well the first entrant served them. Which means getting to the community first, with the right understanding, is itself the defensibility.

Real defensibility comes from three things that compound over time. Vertical depth: the companies that develop genuine domain expertise, AI shaped around the specific workflows, regulations, and relationships of a particular industry, build something that takes years to replicate. Distribution relationships: the trust networks, community positions, and platform integrations that deliver customers become progressively harder to dislodge. And workflow lock-in: when your service replaces the operational habits of a business, switching costs emerge that have nothing to do with features.

This is also why enterprise incumbents extending downmarket represent less risk than they initially appear to. Their cost structures, sales organizations, and product roadmaps are optimized for high-ACV customers. Moving down isn't a product decision — it requires an organizational transformation that cannibalizes the margins their investors have priced in. More fundamentally, horizontal platforms cannot deliver the vertical specificity that the Big Bottom demands. A pet travel compliance engine must integrate with IATA live animal regulations, carrier-specific requirements, and destination-country documentation rules that change without notice. A generalist platform cannot prioritize that depth without it becoming noise for the vast majority of users it doesn't serve. The same structural economics that kept the Big Bottom unserved for decades also constrain the incumbents most likely to notice the opportunity.

What This Requires to Be True

Most analyses of this opportunity isolate one variable and assume the others follow. They don't. Each condition constrains the others.

AI makes service economics work when the system is genuinely agentic. Not AI-assisted humans, but AI that owns the goal and delivers the outcome. The margin only works if you're substituting for a human function, not layering a tool on top of one.

Positioning activates latent demand when it speaks directly to the customer's lived experience and names the pain they've normalized. Not to everyone, but unmistakably to the right person. In a non-consumption market, that's the difference between a business and a product no one finds.

Distribution scales customer reach when it runs through channels that compound through community trust rather than paid spend, reaching people in contexts where self-identification is already halfway done. The channel and the message are one motion. Companies that treat them as sequential functions usually fail at both.

The conditions above are not a build sequence. Most founders treat them as one — ship the product, then figure out positioning, then build distribution. In Big Bottom markets, that sequencing is the failure mode. Positioning done after the product ships is reverse-engineered from what you built, not from what your customer actually needs. Distribution built before positioning locks you into channels carrying the wrong message. And agentic operations built without deep customer knowledge produce efficiency at the wrong task.

The companies that get this right develop all three in parallel, grounded in the same ethnographic base: sustained, intimate engagement with a specific customer before building anything at scale. That's what makes the positioning land, earns the early community trust that becomes distribution, and shapes the AI around the workflows that actually matter. When all three are working from the same customer understanding, they compound. Each makes the others more defensible.

Agentic operations without distribution means a profitable service nobody finds. Distribution without positioning means reaching people who don't recognize themselves as your customer. Both without the economics means the unit math collapses as you scale.

Defensibility isn't built. It accumulates — when all three are working, over time.